JP Morgan TMT: Overview, Deals, and Interview Questions

Published:Given the decline in equity markets so far this year - paired with capital markets that are as quiet as they have been for a decade - you probably won't be surprised to hear that TMT M&A deal volume has fallen quite significantly.

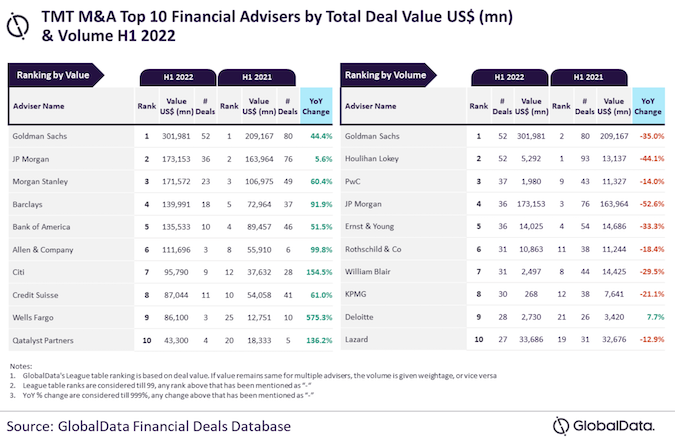

However, what may surprise you when looking at the league table below - which covers the first half of 2022 - is the fact that despite deal volume being down significantly, total deal value is around flat overall (with some firms having seen significant YoY growth in deal value terms).

While this may seem counterintuitive at first, it's easily explainable. When equity prices fall sharply and the animal spirits of the market retreat, that spells trouble for capital market activities but doesn't necessarily mean that all M&A activity grinds to a halt.

In fact, for certain kinds of buyers - sponsors with tons of cash or large strategics with tons of cash - it can be a great time to go hunting for (relative) discounts. However, what these kinds of buyers tend to focus on are large deals with relatively solid financials as opposed to little tack-on acquisitions or pre-revenue growth companies.

So during turbulent times smaller deals - done most often by smaller acquirers - tend to be put on pause and what's left are large deals being done by large acquirers.

This is largely why a bank like JP Morgan has such a relative level of stability. Sure, volumes are down and SPAC activity has more or less entirely dried up (i.e., one of the last gasps being JPM advising FiscalNote). But while those smaller deals have partially evaporated due to evolving market conditions, they've gotten on large deals that aren't as responsive to market conditions. For example, Intel buying Tower Semiconductor isn't something that would change if the Fed hikes another 150 basis points (JPM advised Tower).

Domestically, JPM has broken their TMT advisory practice into two separate groups: tech and media + communications. Historically, media and communications has been an exceptionally strong group. While tech was perhaps a step behind years ago, they've become a very strong group that will get you wide exposure.

People can quibble around the relative prestige of either group. But if you're going through group placement then you should simply opt for whatever group better captures your interest (although it doesn't hurt to always crawl LinkedIn to check out the latest exits that the group has had just to make sure people are going on to do things that are of interest to you).

Some recent deals on the tech side include advising on Take-Two Interactive's acquisition on Zynga for around $14b (JPM advised Take-Two with LionTree, Goldman advised Zynga). More recently, JPM is advising AppLovin on its bid to merge with Unity which will be very intriguing to see play out.

Additionally, JPM has been involved in some interesting semiconductor deals, such as Intel acquiring Tower Semiconductor for $5.4b (JPM advised Tower Semiconductor).

On the telecom side, JPM has a very strong relationship with American Tower (who is a very active acquirer who we wrote about extensively in the TMT guides). For example, JPM is advising American Tower on Stonepeak acquiring a significant stake in their US data center business.

On the media side, JPM rather famously advised on the AT&T acquisition of TimeWarner in 2016. Then, just last year, advised on AT&T spinning off and merging WarnerMedia (the rebranding of TimeWarner) with Discovery after the acquisition proved to not be as accretive (to say the least) as previously thought.

Note: To be clear, when talking about deal activity here we're referring strictly to M&A. Capital markets activity - especially regarding anything touching tech or media - is very quiet and the rise of hung deals is a concerning development.

JPM TMT Interview Questions

Below are a few questions you could be asked through the interview process, especially if you express an interest in either tech or media and communications during your interview. Alternatively, some of these more open-ended questions are what you could be asked while going through the group selection process.

- Let's say that BuyerCo has EBITDA of $300 and TargetCo has EBITDA of $100. When BuyerCo acquired TargetCo, there were $100 in revenue synergies and $50 in cost synergies. What's the pro forma EBITDA? Assume this is a tech acquisition where margins are very high (80%).

- When we think about high-growth SaaS companies, we need to think about MRR. What do you think are some of the key factors that inform MRR?

- Given the sharp decline in equity markets we've seen this year, what do you think this portends for TMT deal flow moving forward?

- Given that many TMT companies have lots of ARR, what will they have a lot more of than companies that bill one-off for their goods or services?

Let's say that BuyerCo has EBITDA of $300 and TargetCo has EBITDA of $100. When BuyerCo acquired TargetCo, there were $100 in revenue synergies and $50 in cost synergies. What's the pro forma EBITDA? Assume this is a tech acquisition where margins are very high (80%).

This is a great technical question because it's a bit off the beaten path. The first thing we'll do here is just add together the two EBITDAs, which will give us $400.

When it comes to the cost synergies, we'll just add the $50 to our initial pro forma EBITDA, giving us $450 overall. This is because you can think about cost synergies as simply reducing pro forma SG&A by $50, which has the effect of increasing pro forma EBITDA by $50.

When it comes to revenue synergies, you can think about them as coming in roughly two forms. Those that are a result of pricing power (i.e., being able to raise prices while keeping COGS the same) and those that are a result of simply selling more goods or services (which obviously means that COGS will go up proportionally with revenue, all else being equal).

If we assume that the revenue synergies are due to pricing power, then we'll simply add the $100 in revenue synergies to the $450 thus giving us a final pro forma EBITDA of $550. However, if we assume that revenue synergies come from selling more goods or services, incurring COGS for each thing sold, then we'll need to strip out COGS (which we're saying in this question is 20% of revenue). So this would lead to a pro forma EBITDA of $530 instead.

When we think about high-growth SaaS companies, we need to think about MRR. What do you think are some of the key factors that inform MRR?

Given that companies with significant subscription revenue have been consistently rewarded by the market with higher multiples, more and more companies have pivoted toward a subscription-first model. This includes even large and established companies like Adobe that made the pivot to a subscription billing model years ago.

Incidentally, Adobe was denigrated by many equity analysts when they made the pivot as these analysts thought the move would be value destructive. However, it's turned out to be quite the opposite.

Anyway, here are the basic factors to consider:

- Retention: How much MRR has been retained from one month to the next.

- Churn: How much MRR has been lost from canceled subscriptions.

- Expansion: How much MRR has been added from existing customers (through upgrading their subscription to a higher monthly amount).

- New Sales: How much MRR has been made from new customers.

- Resurrected: How much MRR has been added by customers signing back up.

- Contraction: How much MRR has been lost by a customer downgrading to a lower priced subscription.

In particular, expansion and contraction are important factors to keep in mind given that most large SaaS businesses will have various "tiers" that customers can upgrade or downgrade to. So during times of economic stress not only will you want to pay careful attention to "churn", you'll also want to pay careful attention to "contraction".

Given the sharp decline in equity markets we've seen this year, what do you think this portends for TMT deal flow moving forward?

This is a classic example of a non-technical question that could be asked during an interview. This is where an interviewee can really separate themselves from others by giving a nuanced and thoughtful answer.

It goes without saying that this question doesn't have an objectively right answer, but there are certainly ways you could answer it poorly (i.e., by saying you expect deal flow to grind to a halt or, even worse, implying that deal flow already has ground to a halt).

So here's how I'd answer this question for interview purposes...

While there's obviously been a sharp downturn in risk assets to start the year - due to the Fed embarking on the most aggressive rate hike cycle of the last four decades - that hasn't caused TMT deal flow to suddenly collapse.

While it's true that deal volume has curtailed significantly, deal value hasn't curtailed nearly as much and large deals are still occurring across media, telecom, and even in the hard hit sector of tech (for example, JPM is currently advising AppLovin on their proposed merger with Unity).

If equity market turmoil continues - whether due to continued Fed hikes or the economy falling into a deeper than anticipated recession - you may see deal volume and deal values continue to fall a bit.

However, there's almost certainly a "floor" to both deal value and deal volume stemming from the reality that there are many groups on the sidelines with significant cash who will be looking to deploy it if valuations fall significantly.

Whether this be private equity funds (i.e., Vista) that have undergone strong fundraising and need to deploy capital on behalf of LPs or whether this be strategic acquirers with strong balance sheets, lots of cash, and a need to continue fuelling growth (i.e., Facebook, American Tower, etc.).

An example of the kinds of transactions that you'll likely see more of moving forward, if the general macroeconomic landscape remains skewed to the downside, would be those like Intel acquiring Tower Semiconductor for $5.3b (JPM advised Tower on the transaction). It's likely the case that Intel was entirely agnostic to current market conditions when deciding to make this acquisition. Instead, they viewed it as essential to their strategic priorities and would have made the deal regardless of where equity markets were, whether the US was officially in a recession, etc.

While it's impossible to truly project where deal flow will be in the future, it's likely the case that tech, media, and telecom will remain reasonably active moving forward -- just not at the incredibly elevated levels seen through most of 2020 and all of 2021. Rather, it's likely the case that the kinds of deals done will be a bit more boring and will predominantly be done by sponsors looking to deploy cash and acquire solid businesses at a discount, or large strategic acquirers who are hunting for accretive transactions that can continue to fuel their growth.

Of course, if inflation abates and economic growth picks up then we could quickly get back to the roaring TMT M&A activity of 2021. However, it's a bit of a contraction in terms to think that inflation will abate from four decade highs while economic growth simultaneously picks up, so don't bet on it!

Given that many TMT companies have lots of ARR, what will they have a lot more of than companies that bill one-off for their goods or services?

They'll have a lot more deferred revenue, which is what you get when you receive cash for goods and services before you actually deliver or render them.

Remember that deferred revenue is a liability because you’re getting cash up front and have the responsibility (liability) of then providing the good or rendering the service at a later date.

For many companies in the tech and media space who have adopted a subscription-based model, they'll provide either a monthly or annual billing option. As you've no doubt observed yourself, the annual option will often offer a significant discount as it, obviously, prevents churn (i.e., having a customer cancel their subscription after a month or two) and creates cash flow certainty for the company. So for companies that prioritize trying to get customers to lock into annual subscriptions, this will lead them to having an even greater amount of deferred revenue.

Another little thing to keep in mind is that when a company operates on a subscription-based model they’ll have lots of current liabilities (as deferred revenue, that will be recognized within a year, will be a current liability) and thus will likely have significantly negative NWC.

Conclusion

Just as we wrote about regarding BofA TMT, the sheer size of JPM's balance sheet means that no coverage group will ever drop too far down the league tables. With that said, the media and communications group has always done very well and the tech group has grown significantly over the past number of years.

Hopefully this little overview and these few interview questions have been helpful. If you want to learn a bit more, we put together a TMT investment banking primer, a media investment banking primer, and a long list of TMT interview questions that you may find interesting.

Note: In case you wanted a more granular breakdown of deal volume and deal activity right now, here's a breakdown from FactSet: