Media Investment Banking: League Table, Subsectors, and Trends

Published:Over the past decade, few companies have faced a greater challenge in pivoting their business models than those that reside within the media and entertainment sectors.

Not only has digitization revolutionized how consumers prefer to engage with content, but the pandemic entirely upended the capacity for some companies in the media and entertainment space to generate revenue for a non-trivial period of time (although, to be fair, some media and entertainment companies, like AMC, were the lucky recipient of meme-stock status and so haven't actually done too poorly).

While those looking to break into investment banking always tend to want to join coverage groups full of companies with rich valuations and strong growth, this isn't all that should be looked for. The reality is that what you want as a banking analyst or associate is to be involved in lots of deals, and generally speaking enhanced volatility in a sector directly translates into more M&A activity occurring.

This can seem counter intuitive at first blush. However, as we'll get into later on in this post, when industries are upended new and enticing business models often emerge. Then an arms race is often unleashed as new entrants and old incumbents try to gobble up market share, which often requires growth by acquisition.

Note: In this post we'll be using "media investment banking" interchangeably with "media and entertainment investment banking". Almost all TMT coverage groups, or those that just refer to themselves as media coverage groups, will also cover companies in the entertainment sector as well.

Media Investment Banking

In this post we'll be trying to relatively concisely give an overview of the media investment banking landscape, along with key media investment banking interview questions you should know. However, the reality is that media investment banking covers an incredibly diverse array of companies - from niche players in radio to large cable companies - so it's impossible to write a few thousands words while giving you a full picture of the media landscape.

Since this post is quite long, you can click the links below to be taken to the parts of the post that are of most interest to you.

- Media Investment Banking League Table

- Media Investment Banking Subsectors

- Media Investment Banking Trends

- Interview Question: What Subsectors of Media do You Think Sponsors are Doing Buyouts in?

Media Investment Banking League Table

As you'd expect, the amount of deal flow and deal activity in media banking is substantially less than in tech. Further, there tends to only be one or two blockbuster deals each year in media. So, as a consequence, who leads the league tables in any given year will be heavily contingent on who gets on those one or two blockbuster deals.

With that being said, there are some media investment banking groups that consistently perform at or near the top of the league table:

- Goldman Sachs TMT

- Morgan Stanley Media & Communications

- Moelis

- Evercore

- LionTree

- J.P. Morgan Media & communications

- Allen & Co

An interesting aspect of media investment banking is the strength of two boutique banks that specialize in media and entertainment: LionTree and Allen & Co. While these are not household names the way Goldman, MS, or JPM are, these are phenomenal places to begin your career if you're primarily interested in media and entertainment. Because the reality is that if you join GS, MS, or JPM you'll get staffed quite often on pitches and deals outside the media space no matter how much you beg your staffer.

While you should never get too caught up in league tables - especially in sectors that can be quite variable year to year - below is a recent league table specifically for large-cap media deals:

Note: The "number of deals" column refers to the number of deals done over a certain size, not all the deals that were done in totality. Also note how the rankings change quite a bit from year-to-year, unlike in tech where things are more stable because blockbuster deals don't tilt the scales nearly as much.

Media Investment Banking Subsectors

Defining what falls within the media sector is increasingly becoming difficult. This is due to a pretty obvious reality: a lot of media companies are now beginning to look a lot like tech companies.

With that being said, if you're ever asked in an interview to rundown the subsectors within media banking you can safely use the following breakdown.

- Advertising: Companies providing advertising, marketing, or public relations services.

- Broadcasting: Owners and operators of television or radio broadcasting systems, including programming. Broadcasting includes radio and television broadcasting, radio networks, and radio streams.

- Cable and Satellite: Providers of cable or satellite television services. Includes cable networks and program distributors.

- Publishing: Publishes of newspapers, magazines, and books in print or electronic form. This includes educational, news, or quasi-news websites.

For the entertainment sector - which is almost always lumped in with media banking - you can safely use the following subsector breakdown:

- Movies and Entertainment: Companies that engage in producing and selling entertainment products and services. Including companies that produce, distribute, or screen movies and television shows; produce or distribute music; movie theaters and entertainment venues; and sports teams. This subsector also includes most companies offering and/or producing streaming content.

- Interactive Home Entertainment: Companies that produce interactive video games. Also includes educational software used primarily in the home.

For interview purposes, you'll never need to have a more granular breakdown than this. What's listed above broadly covers almost every possible company you'd be covering as a media banker.

Media Investment Banking Trends

If you're ever in an interview and profess an interest in media and entertainment, you'll likely be asked about a trend you're following. If you really want to impress your interviewer, it's always a great idea to talk about a trend and then talk about how a recent deal has exemplified that trend.

Given that there are almost no group of companies that have been as heavily disrupted over the past decade - due to both technological changes and the pandemic - than those in media and entertainment, there are a number of potential trends you could talk about.

- The continued persistence of cord-cutting and how that is affecting cable and satellite operators.

- The rise of streaming services and the arms race taking place to get as much original content (or exclusive rights to old content) as possible.

- How SPACs are allowing media companies with iffy financials (e.g., Buzzfeed, potentially VOX) to finally go public.

- The disruption of the classic theater release schedule and how this is altering the economics of producers and distributors of films, along with theaters themselves (meaning: movies are now being released DTC and in theaters on the same day, or being released DTC shortly after their theatrical release).

- The rise of sponsors (PE funds) buying up quasi-distressed or underperforming media assets (Apollo is actively doing this). Alternatively, sponsors doing buyouts of healthy media companies with relatively stable and predictable cash flows (sponsors used to be quite a bit less active in the media and entertainment space primarily due to how quickly consumer tastes can change).

So, for example, you could talk about the rapid rise of streaming services from both classic media companies and from the tech giants (e.g., Netflix, Disney+, Amazon Prime Video, HBO Max, Paramount+ for CBS, Peacock for NBC, and ESPN+).

The appeal behind creating a streaming service is obvious. If you can get enough scale, it can provide phenomenal recurring revenue that the market always values at a high multiple.

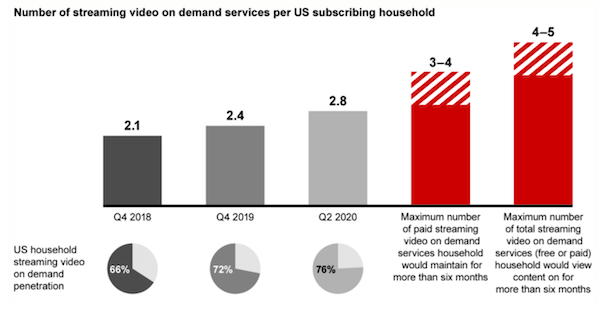

However, while streaming is not entirely zero sum, it does appear as though there is an upper bound to how many individual streaming services consumers are willing to sign up for and keeping paying for. As of now, the average consumer pays for approximately three streaming services and the average limit on how many they'd ever sign up for and keep paying for is 3-4.

This reality has created a kind of arms race whereby every streaming service is shelling out ever greater amounts of money on creating their own original programming and on buying the rights to previously popular TV shows or movies. In the end, all the streaming services understand they can't all be viable in the long run so they must try to rapidly grow their market share and outlast their competitors.

A recent deal that exemplifies this trend is Amazon's acquisition of MGM for an enterprise value of $8.45b. Chances are you've already heard of Metro-Goldwyn-Mayer or at least seen their iconic logo flash in the opening credits of a movie. They're a large studio that has a catalogue of over 4,000 movies - with titles such as James Bond - and over 17,000 TV episodes (with titles such as Survivor).

You can think about the strategic rationale for this acquisition as having four components:

- The acquisition will allow Amazon to deepen its content catalogue compared to its two closest comparables that have much larger libraries currently (Netflix and Disney+)

- The acquisition will help reduce churn by introducing loads of fresh content to subscribers (which they can drip feed in over time)

- The acquisition comes along, obviously, with the studio itself and all the human capital and institutional knowledge contained within it; this will help Amazon more rapidly expand out its ability to create original programming

- The acquisition will preclude someone else (e.g., Disney, Netflix, etc.) from buying MGM and locking in that content library for itself

Reportedly, MGM had just ~$173m in 2020 EBITDA, putting the EV multiple of the deal at an eye-watering 49x. Needless to say, MGM wouldn't have been picked up for even a fraction of this multiple five or ten years ago.

However, MGM has the content and the content creation capacity that is suddenly a hot commodity for those looking to win the streaming arms race. Also, just to put things in perspective, Amazon spent $7b on content creation alone in 2020. So, MGM isn't that big of an acquisition when viewed through just how much content and content creation capacity Amazon is getting.

Note: Another big studio deal, that occurred prior to when the streaming wars really heated up, was Disney acquiring 21st Century Fox for $71b at a 13x multiple.

Interview Question: What Subsectors of Media do You Think Sponsors are Doing Buyouts in?

A common question to be asked in interviews that indirectly gets at whether you understand the scope of the media industry and the priorities of sponsors (PE funds) is what sub-sectors of media you think sponsors are doing buyouts in.

Because, as you can imagine, just as PE firms are largely uninterested in doing buyouts of traditional semiconductor manufactures in the tech sector, they're also largely uninterested in doing buyouts of certain kinds of media companies.

It's best to always begin your answer by generally laying out what sponsors are looking for in a buyout target (regardless of the industry we're talking about). The three basic things they're looking for are companies that have reasonably predictable cashflows, that don't require large future capex spending, and that will allow the sponsor to flip the company after a five to seven year holding period.

It may surprise you to know that the entertainment industry has been a slightly active area for sponsors in recent years. For example, Blackstone was part of a buyout of Merlin Entertainment, which holds Legoland and Madame Tussauds, for $7.5b in 2019.

While you may think that the pandemic will curtail any interest by sponsors in the entertainment space, keep in mind that with valuations across all sectors being quite rich the entertainment sector is one where valuations are still relatively low. Further, many entertainment companies have significant intellectual property that has value distinct from the core operating business, and sponsors may believe this IP isn't being properly monetized.

With all that being said, sponsors have consistently been active in the publishing sub-sector of media. The perfect example of a publishing buyout is McGraw Hill, which is the publisher of overpriced textbooks and whatnot that you probably bought in college. Platinum Equity acquired McGraw Hill from Apollo for $6.7b in enterprise value ($4.5 in equity value). This is an example of a sponsor-to-sponsor or cross-fund transaction, which you may be surprised to know is increasingly common to see.

Conclusion

By working in media M&A you'll get a front row seat to the massive upheaval and disruption occurring in the industry. From how cable and satellite operators are trying to stave off cord-cutting and reinvent themselves, to how Hollywood studios are adapting to the radically altering economics behind film production and distribution.

As hopefully this post has been able to illustrate, the media and entertainment sectors are incredibly diverse. Including everything from radio broadcasters to theme parks.

Part of what makes media investment banking so interesting is that every media company derives most (if not all) of their revenue directly from consumers. And given how fickle consumers can be this requires companies to be constantly evolving, constantly testing new markets, and constantly trying to grow through acquisition if at all possible. If you're a media company, you can't just stay still or else you will be disrupted (it's not a matter of if, but when).

While some look at the level of deal activity and deal flow in the media space and think it must be a bit sleepy, it's anything but that. Further, if you're really sold on media and entertainment banking there are great boutiques out there where you can focus almost exclusively on doing just media and entertainment deals.

If you're looking for more interview questions, we've compiled a longer list of TMT interview questions here (keep in mind that most questions that you'll be asked in any investment banking interview will be classic technicals). We also put quite a bit of time and effort into creating dedicated TMT interview guides, including one just for media banking, which you can also check out if you're interested.

Hopefully this has piqued your interest in media investment banking. If you'd like us to do any more granular write-ups, feel free to let us know.