TMT Investment Banking: Tech, Media, and Telecom Primer

Published:It's no secret that Tech, Media, and Telecom (TMT) has been the most watched M&A sector over the past decade. While many think of TMT as being quite a volatile sector - because it encompasses many high-flying tech startups with eye-watering valuations - in terms of M&A deal volume and deal value it has actually quite steadily grown over the past decade without much aberration.

Today, TMT is the largest and most active M&A sector by quite a large margin. In fact, in 2021 alone TMT M&A deal volume has easily cleared $1 trillion, and forecasts show that 2022 will likely be as strong if not stronger.

Note: Total M&A deal volume in 2021 hit $5 trillion, with TMT representing roughly 25% of total deal volume (which no doubt helped spur the sharp rise in junior banking salary and bonuses we saw in 2021-2022).

The persistence of TMT as the leading M&A sector over the past decade is largely a reflection of three factors:

- The increasing digitization of the entire economy. Increasingly every company, regardless of if their primary business is oil and gas extraction or asset management, needs to have significant tech capabilities (thus they may acquire tech companies to onboard talent and technology instead of developing it internally)

- As the valuations for companies in the TMT sector have rapidly grown - with some exceptions, like for some companies within the media space - this has given companies within the TMT sector the ability to more aggressively acquire other companies. Thus creating a virtuous circle whereby increasing valuations in the TMT sector leads to more TMT deal activity, which in turn often leads to higher TMT valuations.

- Finally, one of the primary stabilizing forces within the TMT M&A space over the past five years has been the rise in PE firms (sponsors) getting involved in doing buyouts.

This last point is incredibly important to understand. When looking at any industry - form an M&A vantage point - what you will find is that the more active that sponsors are in the space, the more stability there will be in deal activity from quarter to quarter.

This is because while strategic acquirers tend to get spooked during bear markets and are often focused on only companies that are accretive to their strategy, sponsors are more than happy to acquire companies during bear markets and are largely strategy-agnostic so long as it fits their investment criteria.

This is all a long-winded way of saying that sponsor involvement in any sector acts as a great stabilizing force. It also, obviously, increases the number of buyers that can be approached when investment bankers are working on a sell-side mandate, which also almost always bumps up the price that a given company will end up going for.

The rise of sponsors in the TMT space is actually quite a recent development. While there have been tech-focused sponsors - like Vista and Thoma Bravo - for several decades, many sponsors five years ago or more were a bit spooked by the high valuations of tech companies and the perceived instability of their cash flows.

However, the reality today is that nearly every PE firm will at least look at companies in the TMT space. This is largely a reflection of how sponsors have gotten more comfortable with the way in which tech companies earn their revenue. Because while there are limited traditional assets underpinning tech companies, they can throw off stable and predictable cash flows that are incredibly enticing to sponsors.

Over the past decade many have viewed TMT investment banking through the lens of the dot-com bubble; thinking that the recent level of M&A deal volume and deal value was a sort of aberration from the norm.

However, the reality is that from an M&A perspective, TMT is one of the least volatile sectors. While natural resources and healthcare banking go through boom and bust cycles when it comes to deal volume, TMT consistently chugs along growing each year thanks to how diverse and large the space has become.

This should be pretty intuitive as you'd expect there to be the most M&A activity in the area of investment banking that deals with companies that most directly affect our lives. And who could argue that all of our lives increasingly revolve around companies within the technology, media, and telecom space?

TMT Investment Banking

This will be quite a long post, so we've broken it down into a number of different sections so that you can easily navigate it. Feel free to click on any of the links below to be taken to a specific part of this post.

TMT Investment Banking Subsectors

TMT Investment Banking Exit Opportunities

Best TMT Investment Banks

One of the unique aspects of TMT - relative to other coverage groups such as healthcare or natural resources - is that it is composition of several quite distinct and large sectors (tech, media, and telecom).

As a result, it's actually somewhat difficult to create a truly accurate TMT league table across all leading investment banks as it would need to adjust for the fact that Morgan Stanley, for example, breaks out media and communications banking from technology banking. This begs the question of whether or not you should combine Morgan Stanley's M&C and tech banking groups together, or if you should think of them each independently.

If you're preparing for TMT interviews, the reality is that you shouldn't concern yourself with the minutia of league tables too much. Instead, you should just make sure that the bank you're applying to has solid and stable deal flow in the area of TMT that most interests you, which in turn will lead to solid and stable exit opportunities.

So, for example, the following is the technology investment banking league tables for 2021 (thus far). As will be the case almost every year, you have Goldman Sachs, Evercore, J.P. Morgan, and Morgan Stanley in the top five (Bank of America fluctuates a bit more year-to-year).

To drive home the point that league tables shouldn't be all that you pay attention to, Qatalyst is ranked in the tenth position currently. However, if you're interested exclusively in tech banking there is hardly a better place to be and folks routinely take offers from Qatalyst over Goldman or Evercore.

Moving on to telecom, we're dealing here with a much smaller set of deals and a much smaller level of deal value. While sponsors do play around in certain areas of telecom - such as buying infrastructure assets - the reality is that most deals will be large in value and between strategics (thus leading to heavily fluctuating league tables year-to-year).

As is most often the case, Goldman and JPM leads the league tables. Of note is that you have both LionTree and Allen & Co on here who are also very strong in media banking, but less so in tech banking (especially for Allen & Co).

Within media investment banking, deals of substantial size occur quite infrequently. So league tables heavily fluctuate based on who ended up getting a mandate on the few blockbuster deals of that year. Generally speaking - as discussed in the media investment banking post - you'll have Morgan Stanley, Evercore, Moelis, JPM, and LionTree leading the way.

Notably two boutique investment banks - LionTree and Allen & Co - will almost always rank in the top ten within media investment banking despite their small size (similar to how Qatalyst is almost always within the top ten for tech deals).

So, in our view, the best way to get a feel for a bank is to look at where they land on the league tables for tech, media, and telecom individually (as opposed to some amalgamated TMT league table). Not only because some very strong banks, like Morgan Stanley, don't have a unified TMT group. But also because some banks - like Qatalyst, Liontree, or Allen & Co - are not active in all areas of TMT by design (thus they would have artificially low rankings in any combined TMT league table).

What has been written above should give you a good sense for the relative strengths of banks across tech, media, and telecom. As you can tell, some banks are quite strong across all three of the sectors that comprise TMT (e.g., MS, Evercore, JPM) while some banks are incredibly strong in one area but not the others (e.g., Qatalyst in tech). With all that being said, if you have an offer from any bank within the top ten of the league tables shown above then rest assured there will be more than enough pitches and deals to keep you (very) busy.

TMT Investment Banking Subsectors

The TMT space is unbelievably diverse; covering everything from cell tower operators, to advertising agencies, to social media platforms. This is why many bulge bracket investment banks - like Morgan Stanley - have created two separate groups, one covering media and telecom and one covering tech.

As we've covered elsewhere on this site, one common question you can get asked in TMT investment banking interviews is to quickly give a rundown of the sectors within tech, media, or telecom.

This may seem like a bit of an odd question to ask, but the reality is that most of those interviewing are exclusively interested in internet / software companies and have zero idea about the diversity of companies covered by tech banking (never-mind what types of companies are covered in media or telecom banking).

So, let's do a quick rundown of all the major subsectors of tech, media, and telecom.

Within media investment banking, you have the following subsectors:

- Advertising: Companies providing advertising, marketing, or public relation services.

- Broadcasting: Owners and operators of television or radio broadcasting systems, including programming. This subsector includes radio and television broadcasting, radio networks, and radio streams.

- Cable and Satellite: Providers of cable or satellite television services. This subsector includes cable networks and program distributors.

- Publishing: Publishers of newspapers, magazines, and books in print or electronic format.

- Movies and Entertainment: Companies that engage in producing and selling entertainment products and services. This subsector includes companies engaged in production, distribution, and screening of movies and television shows; producers and distributors of music; movie theaters; sports teams; and streaming visual or audio services.

- Interactive Home Entertainment: Producers of interactive gaming products, including video games. This subsector also includes educational software used primarily in the home.

As you can imagine, for many companies it's a bit ambiguous as to whether they are truly a tech company or a media company. Generally whenever there's ambiguity companies argue that they're tech companies in the hopes of getting higher multiples applied to them by the market.

Within telecom investment banking, you have the following subsectors:

- Wireless Telecom Service Providers: Companies that exclusively provide cellular or wireless telecom services.

- Convergent Telecom Service Providers: Companies that operate fixed-line telecom networks for wireless along with internet access.

- Alternative Carriers: Companies that operate fiberoptic and/or high bandwidth cable for data transmission.

- Data Centers and Infrastructure Providers: Companies that provide services and infrastructure to enterprise clients (data centers, cloud networking, storage infrastructure, and web hosting). Also includes, importantly, cell tower operators.

Within tech investment banking, you have an incredible amount of diversity and you can get quite granular with the subsectors. However, a simple list that broadly covers almost everything is as follows:

- IT Services: This is quite a diverse subsector, but you can think of this as involving companies that provide help to other businesses surrounding tech support, outsourced software development and staffing, and IT integration. Basically, companies in this area are like consultants who help companies that don't have much internal IT capacity.

- Software: You can think of the software subsector as involving companies that are selling either vertical, horizontal, or infrastructure software.

- Internet: This is the broadest subsector of tech banking (as the name implies), and covers everything from ecommerce to search to marketplaces to online gaming. This subsector basically covers any company that lives on the internet, but that can't be considered software.

- Hardware: The hardware subsector involves basically everything physical that's associated with technology; from communication equipment, like routers, to everything that comprises a tech-enabled product (with the exception of semiconductors).

- Semiconductors: The semiconductor subsector can be broken down more granularly into four additional subsectors (that are covered in the Tech Investment Banking Guide). The bulk of semiconductor revenue stems from microprocessors and logic devices, along with memory devices. As you no doubt already know, the semiconductor industry is quite concentrated given the huge amount of capex that goes into developing fabs (semiconductor fabrication plants), along with the general R&D expense involved in bringing new types of semiconductors to the market.

As you can no doubt tell, TMT covers a vast swath of wildly different companies. Hopefully the above gives you some sense for this scope, although we could take a few thousand words to break down each one of these subsectors further.

The important thing to realize is that what many think of first when they think of TMT (FAANG) actually makes up just a sliver of what kinds of companies are covered.

TMT Trends in 2022

Every year brings on a new set of trends within TMT that everyone will be talking about. However, the reality is that given the incredibly diversity of the TMT space there are multiple micro trends within every subsector.

With that being said, below are some overriding trends that we believe will inform deal activity within the TMT space in 2022 and into 2023. Given that we don't want this post to grow too unruly, we'll try to be a bit brief on each of these points. But if you're interested in our thoughts on any of these, feel free to let us know and we'll try to do a follow-up post at some point.

The Continued Rise of Sponsors

As we briefly touched on earlier, five years ago or so it was much less common to see sponsors (PE funds) actively doing buyouts in the TMT space.

While there have always been some PE funds - like Vista and Thoma Bravo - that have specialized in tech buyouts, most sponsors were a bit reticent to touch companies that didn't have the traditional asset base of a company in other sectors (e.g., consumers or industrials).

However, over the past five years three major things have happened.

- First, sponsors have become much more comfortable with the economics underpinning tech companies (in particular, software companies with recurring revenue).

- Second, with so much money pouring into PE funds, there is an incredibly limited pool of companies to buyout if one refuses to look at the TMT space (meaning: too much money chasing too few potential deals).

- Third, lenders have become much more comfortable working with sponsors on TMT buyouts (even if the target companies often have an asset light balance sheet and a slightly unorthodox looking income statement).

In the below graphic you can see deal volume (for $1b+ transactions) by strategics vs. sponsors within the tech sector. As you can see, sponsors are much more active than they were a decade ago.

Sponsors aren't just focused on tech either. Within the telecom space, one of the key drivers of deal activity in 2021 has been sponsors snatching up infrastructure assets (cell towers), which have everything that a sponsor is looking for: low maintenance capex, sticky clients, and strong recurring cashflows.

Within the media space, there's also been some interesting deals over the past few years. For example, one that may surprise you is Blackstone taking Merlin private for $7.5b (Merlin owns a few parks like Legoland, etc.).

Cord Cutting and the Streaming Wars

The rise of cord cutting and the subsequent onset of the "streaming wars" is a theme that touches a number of different types of companies within TMT; from cable and satellite operators, to big tech companies, to movie studios, to theaters.

Currently, nearly everyone tangentially involved in the production or distribution of television shows or movies is having to rethink their business model in light of what the future could bring. This began well before the pandemic with the rise of cord cutting, but has only been exacerbated by it since.

While this trend likely deserves a post unto itself, let's cover some basics here.

First of all, as you no doubt already know over the past few years nearly everyone with some form of content library has put out a streaming service. Both in order to insulate themselves from their legacy business being disrupted (e.g., Discovery+) or to try to unlock some much coveted recurring revenue by further monetizing their intellectual property (e.g., Disney+).

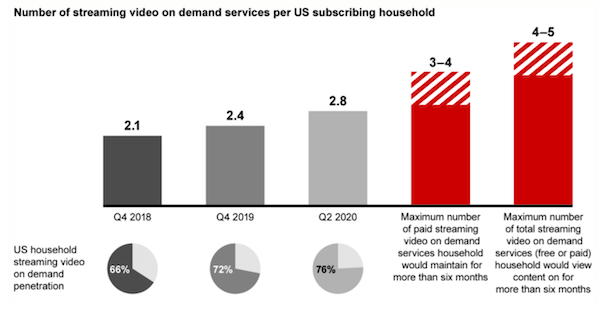

At present, within the United States, these are the major streaming services offered: Netflix, Amazon Prime Video, Hulu, CBS All Access, HBO Max, Discovery+, ESPN+, Disney+, Paramount+, and Peacock.

However, there's an issue: consumers have a limit to just how many of these services they're willing to subscribe to long-term.

This reality has given rise to the term streaming wars; reflecting the fact that while having tens of millions of consumers paying you $5-15 a month is fantastic, not everyone will be able to achieve that reality.

Instead, what streaming providers need to do is compile the largest content library possible, keep churning out new content that satisfies consumer demand, and hope they can gain a significant amount of market share and squeeze out competitors.

To that end, we've seen a large uptick in media M&A activity over the past few years as large telcos and big tech companies have been fighting to secure the rights to content libraries and to buy studios to help be able to produce content at a faster clip.

One of the best examples of this lately is Amazon acquiring MGM - which has a library of over 4,000 movies and 17,000 TV episodes - for an EV of $8.45b, which represents a reported 49x EBITDA multiple. This acquisition will help broaden out Amazon Prime Video's content library - which is quite a bit more sparse than Disney's or Netflix's - while at the same time giving it yet another studio to help churn out content from.

Amazon's acquisition isn't exactly novel. In 2019 Disney acquired the much larger 21st Century Fox for $71b. In fact, even sponsors have kind of got into the game with Blackstone acquiring the production company Hello Sunshine, which was founded by Reese Witherspoon (this was a relatively small and somewhat nuanced deal, to be fair).

The rise of cord cutting and the ensuing streaming wars have been a trend for the last several years, and it shows no sign of slowing down. In the end, volatility in sectors almost always results in enhanced M&A activity. Either because some companies are growing very quick, so can use their high equity value to partially fund acquisitions, or because incumbents know they need to pivot in order to survive the disruption that's occurring.

Note: One of the most impactful, complex, and (some think) disastrous M&A deal of the last decade - AT&T acquiring Time Warner for $85b - was done largely due to the disruption seen from cord cutting and the rise of streaming platforms. It was a protective maneuver that simply didn't work out, and now AT&T is unwinding its acquisition in yet another strategy pivot. We get into this more in the Tech Guide, because it requires a few thousand words to fully convey what happened and why it's so indicative of the changing media landscape.

Other Trends

Of course, there are many, many other trends we could discuss. A quick listing of a few more are below:

- The rise, fall, and (potential) rise again of SPACs

- The enhanced demand among sponsors and strategics alike for telecom infrastructure assets

- The pivoting of satellite operators to abate cord cutting

- The changing release window for movies and the subsequent impact on theaters

- How rising rates could impair the valuations of pre-revenue high-growth tech companies

- Ecommerce stickiness as the economy continues to re-open

TMT Investment Banking Exit Opportunities

Talking about exit opportunities as it relates broadly to a given coverage group is a bit tricky. Because at the end of the day it still matters where you worked, not just what you worked on.

However, as a general principle, if you've got an investment banking offer to a bank but are completely agnostic on which group you'd like to join, then it's a great idea to choose TMT.

This is for two separate reasons.

First, given the high level of deal activity within TMT, no matter what bank you join you'll probably get a not trivial level of deal exposure (and it's always important to have closed deals on your resume).

Second, given the fast growth of TMT over the past decade, there are loads of corporate development style roles that will be available to you if you want to leave high finance (whereas those who joined FIG, for example, may be more limited on the corp dev side unless they were at a well-known top group like Goldman FIG).

Now it should go without saying that within a top TMT group - like Goldman's - virtually every style of traditional banking exit opportunity will be available to you.

So, if you wanted to go join a mega fund PE firm, you could. Likewise, if you wanted to join a long-short hedge fund, or a venture capital fund that routinely takes bankers, then you could as well. Likewise, if moving outside of high finance after banking is appealing to you, then you can absolutely go into almost any kind of corporate development role you'd like to (again, so long as they normally take bankers).

Needless to say, as you move down the prestige hierarchy your exit opportunities will shrink a bit. The vast majority of corporate development roles will still be open to you, but those within high finance will change a bit. Well regarded long-short hedge fund opportunities and mega fund private equity opportunities will, with some exceptions, be replaced more with middle market and lower middle market private equity opportunities.

Again, this is all a bit of a generalization. However, one thing that has become readily apparent over the past year is that fewer people at top groups across banking - but in particular within TMT - are sticking around high finance. An increasing proportion are taking quite high paying corp dev roles within big tech, starting their own companies, or heading off immediately to business school.

In fact, many at top groups aren't even sticking around banking until on-cycle recruiting happens, but instead are leaving for the first enticing corp dev style role that they can land. This, in turn, has lead to many at "lower prestige" groups getting offered hedge fund and private equity roles they would in years past not have been able to land an interview for.

Anyway, we don't want to belabor this point too much (although we can delve a bit deeper in future posts if you'd like). Suffice to say that by joining a TMT group you will open yourself up to as full a slate of exit opportunities as any other group within your bank would (with the exception being when a bank has a singular group it's really well known for, and a TMT group that is a bit lackluster).

Note: It should be added that if a bank breaks out tech from media and telecom, then the tech group almost always has stronger deal flow and exits than the media and telecom group will. Again, this is a bit of a generalization however.

Conclusion

There is no group within investment banking as dynamic and diverse as tech, media, and telecom. Whether you're looking for exposure to SaaS companies with mind-numbingly large valuations or cable operators with tens of millions of customers, you'll get it within TMT.

With that being said, it can take some time to fully get your arms around what kinds of companies are covered by TMT bankers, how they're valued, and who the acquirers tend to be.

Hopefully this post has given you a helpful glimpse behind the curtain. If you're currently gearing up for interviews, you should be prepared for relatively intensive interviews given the popularity of TMT. This is why we put together a reasonably long list of TMT investment banking interview questions. Additionally, we also put together guides on tech, media, and telecom - along with guides on advanced accounting and valuation technicals - to help solidify your understanding if you think that'd be helpful.

TMT has not only been the hottest area of investment banking over the past decade, but will almost certainly be the hottest area of investment banking over the next ten years. Even if you aren't directly interested in the kinds of companies that are covered within TMT, it's worth thinking deeply about the trends affecting TMT as they tend to permeate outwards and similarly touch every industry.